Dr. Lawrie has provided a rapid review to validate the analysis of efficacy of Ivermectin provided by the Frontline Covid-19 Critical Care Alliance , based in the US. Its leading figures have recently given testimony to the National Institute of Health’s Covid-19 Treatment Panel In New York. In connection with her analysis of ivermectin she sent a letter to Health Secretary Mr. Hancock and other MP’s on 3 January and has so far received no reply.

In her letter to the Prime Minister Dr. Lawrie states,

“The good news is that we now have solid evidence of an effective treatment Covid-19. It is called ivermectin. Ivermectin is a very safe and effective anti-parasitic medication widely used in low and middle income countries to treat worms, lice and scabies in both adults and children. It has been around for decades and not only is it on the WHO list of essential medicines it is a Nobel Prize winning medicine due to its increasing usefulness across a range of illnesses.

Between Xmas and new year I independently reviewed 27 studies presented by the FLCCC as evidence of ivermectin effectiveness. The resulting evidence is consistent and unequivocal : ivermectin works well both in preventing covid infections and in preventing deaths at the same doses used to treat lice other parasitic infections.

I am very pleased to inform you that this evidence solidly substantiates the FLCCC’s recommendation that ivermectin should be adopted globally and systematically for the prevention and treatment of Covid-19. Because I know there is alot of fake news going about I would like to assure you that you can trust the integrity of my report because I am an experienced independent medical research consultant whose work is routinely used to underpin international clinical practice guidelines. In addition I have no conflict of interest and have received no funding for this report.

But most of all you can trust me because I am a medical doctor first and foremost with amoral duty to help people, to do no harm and to save lives.

Please may we start saving lives now.

Thank you very much for your help. Mr.Hancock’s office should have my details. ”

Treasury Secretary Janet Yellen said Friday that she hopes President Joe Biden’s $1.9 trillion coronavirus stimulus package will help bring back full employment by 2022. Speaking with PBS NewsHour, Yellen said the U.S. needs to “go big” with coronavirus relief in order to help get the economy back on track to pre-pandemic levels. “It’s a big [stimulus] package, but I think that we need to go big now, and that we can afford to go big,” she said. “And the most important thing is to get our economy back on track and help people get their lives back, in order to make sure that this pandemic doesn’t permanently scar our work force. And I think this is what we need. I’m hopeful that, next year, with a package of this size, we can be back at full employment.” Yellen’s comments came after Friday’s announcement that the U.S. economy exceeded expectations by adding 379,000 new jobs in February. While Yellen said she was “pleased” with those numbers, she added that the unemployment rate is still running at about 10 percent. “When you think about the pace, although 379,000 jobs in one month, it sounds like a lot,” she said. “But, at that pace, it would take us more than two years to get back to full employment. And we’re — we want to make sure that our workers get back to full employment, the state we had in the economy before the pandemic struck, a lot sooner than that.” “The package that the president and his advisers put together that’s working its way through the Senate now was really geared to relieve the suffering of the American people,” she added. Biden’s stimulus package, called the American Rescue Plan, was passed by the House of Representatives on February 26 and has now been passed in the Senate. The package now goes back to the house where the Senate version of the bill is reconciled against the House version. It is expected to with little change.

United States President Joe Biden said on Saturday that the coronavirus stimulus bill, which was approved by the Senate earlier in the day, “proved that this government, this democracy, can still work.” He pointed out the bipartisan support the package received in opinion polls, although no Republican senators voted in favor of it. “Everything in this package is designed to relieve the suffering and to meet the most urgent needs of the nation and put us in a better position to prevail,” Biden stated. He added that the stimulus will create an estimated six million new jobs, increase the gross domestic product by a trillion dollars and “put our nation in a position to outcompete the rest of the world.”

Senate Democrats passed President Biden’s $1.9 trillion American Rescue Plan on Saturday afternoon in a 50-49 vote after a grueling all-night voting session, pushing the massive relief bill over a crucial hurdle on its way to becoming law over the objections of the Republican Party and setting up a major victory for Biden in the early days of his presidency. The legislation will authorize hundreds of billions of dollars in federal spending for vaccine distribution and virus testing, hospitals, state and local governments, schools and small businesses to combat the ongoing coronavirus pandemic and offset its economic toll.

The bill includes a third round of stimulus checks in the amount of $1,400 for eligible individuals, another tranche of enhanced federal unemployment benefits of $300 per week, a major expansion of the child tax credit, tax relief for canceled student loan debt and billions of dollars for rental and food assistance.

Provisions like those, which are designed to provide direct aid to American families struggling to stay afloat amid the slowdown, prompted Senate Majority Leader Chuck Schumer (D-N.Y.) to predict that the legislation will be the “single largest anti-poverty bill in recent history.” Republicans widely oppose the package: they say it is too expensive, describe it as unnecessary given the pace of economic recovery and object to provisions they view as unrelated to the coronavirus crisis. Some economists and lawmakers have suggested the bill’s $1.9 trillion price tag could trigger dangerous inflation and destabilize the nascent economic recovery, but Biden’s White House and top Democrats have consistently said “big” spending is warranted given the sheer scale of the crisis. During a brutal legislative process called a “vote-a-rama” that dragged for more than 24 hours on Friday and Saturday, Democrats defeated a slew of GOP amendments to the bill, including a bid to replace the entire package with a $650 billion version instead and attempts to bar undocumented immigrants and incarcerated individuals from receiving stimulus checks. 9.5 million workers are still unemployed in the United States, according to data released Friday by the Labor Department, despite job growth that exceeded economists’ expectations in February. Democrats used a special legislative process called budget reconciliation to pass the bill with only a simple majority of votes rather than the usual 60 required to overcome a filibuster in the Senate. Since Democrats hold exactly 50 seats in that chamber (with Vice President Kamala Harris breaking a tie in their favor), they could not afford to lose a single vote. That razor thin majority prompted changes to previous versions of the bill in order to appease moderates within the caucus. After hours of fraught negotiations on Friday, Democratic leaders cut a deal with Sen. Joe Manchin of West Virginia, a conservative Democrat, to scale back the next round of enhanced federal unemployment benefits to $300 per week through September 6 rather than the $400 per week supplement many Democrats favored. They also scaled back eligibility requirements for the $1,400 stimulus checks—a major concession to moderates like Manchin who want to prevent high earning families from receiving federal relief they don’t need and aren’t likely to spend. The package will now be sent back to the House of Representatives so that chamber can approve the Senate’s changes. After that, President Biden will be able to sign the bill into law. Democratic leaders have repeatedly expressed confidence Biden will sign before March 14, when the enhanced federal unemployment insurance authorized by the last stimulus bill will expire and 11.4 million Americans will lose their benefits. If the $1.9 trillion American Rescue Plan is enacted, it will be the sixth federal rescue package signed into law since the onset of the coronavirus pandemic in the United States last year. Whether the changes the Senate made to the bill will imperil its final passage in the House, where progressives were already bristling over the Senate’s decision to strike the minimum wage hike from the package. House Speaker Nancy Pelosi (D-Calif.) has said the chamber will “absolutely” pass the package without the $15 minimum wage.

Wall Street markets extended gains on Friday towards the end of the last session of the week as details of the $1.9 trillion stimulus bill were making headlines. Although the Senate had voted earlier to not add the $15 minimum wage to the relief package, US President Joe Biden said it is still a priority for him to make it happen.Dow Jones jumped 515 points or 1.67% at 2:59 pm ET, while Nasdaq 100 gained 212 points or 1.69% at the same time. S&P 500 added 67 point.

The 10-year United States Treasury yield is now returning to the levels it last had six months before the coronavirus pandemic, as the economic outlook improves overall, St. Louis Federal Reserve Bank President James Bullard said on Friday. The better economic expectations are bringing real yields higher, he noted but also added that the 10-year yield level is still quite low. The 10-year yield hit highs last seen in October 2019 and was at 1.561%, rising by 1.1 basis points at 12:37 pm ET. Commenting on inflation, Bullard stated that he would support a 2% inflation target on a sustained basis.

Federal Reserve Chairman Jerome Powell “there is no plan to raise interest rates until labor-market conditions are consistent with maximum employment and inflation is sustainably at 2%.”

WASHINGTON—Federal Reserve Chairman Jerome Powell reiterated his intention to keep easy-money policies in place but provided no sign the central bank will seek to stem a recent rise in Treasury yields, prompting them to rise further. Stocks also sold off on Mr. Powell’s remarks Thursday during an interview at The Wall Street Journal Jobs Summit. The appearance came a week after a jump in Treasury yields driven by forecasts of stronger U.S. economic growth and inflation this year, among other factors. “Today we’re still a long way from our goals of maximum employment and inflation averaging 2% over time,” Mr. Powell said Thursday during the interview.The Covid-19 pandemic continues to upend the job market. Some analysts said his latest remarks did little to ease investor fears about rising bond yields.“The market was looking for some more reassurance and didn’t get it,” said Krishna Guha, head of global policy and central bank strategy at Evercore ISI. Fed officials “don’t appear particularly concerned about the current level of yields, which in both real and nominal terms is significantly higher than it was two weeks ago.” The yield on the 10-year Treasury note rose above 1.55% after Mr. Powell’s interview—its highest level since before the pandemic—up from 1.46% earlier Thursday and 0.92% at the beginning of the year. The Dow Jones Industrial Average lost 345.95 points, or 1.11%, to 30924.14 Thursday. The S&P 500 declined 51.25 points, or 1.34%, to 3768.47, the third consecutive session of declines. The Nasdaq Composite fell 274.28 points, or 2.11%, to 12723.47. Meanwhile, oil prices rose Thursday after OPEC and a Russia-led coalition of oil producers kept most of their production cuts in place, surprising traders who had expected the group to increase output. Mr. Powell’s remarks came at his last scheduled public event before Fed policy makers meet on March 16-17. He said the central bank will maintain ultra-low interest rates until its employment and inflation goals have been met, and will continue hefty asset purchases until “substantial further progress” has been made. Recent evidence suggests the labor market is improving, but slowly. The Labor Department said Thursday that filings for unemployment benefits, a proxy for layoffs, rose slightly to 745,000 in the week ended Feb. 27, down from 927,000 in early January but more than three times their pre-pandemic levels. Mr. Powell noted that the U.S. has about 10 million fewer jobs than before the pandemic and said, “It will take some time to get back to maximum employment.”The central bank has held its overnight federal-funds rate near zero since last March. It has sought to suppress longer-term rates by purchasing, since last June, at least $120 billion a month of Treasury debt and mortgage-backed securities. As bond yields have risen, some investors have begun to speculate that the Fed could start to skew its asset purchases or holdings toward longer-dated instruments in order to keep borrowing costs low. Asked Thursday about the climb in long-term rates, Mr. Powell said it “was something that was notable and caught my attention.” But he signaled no imminent policy response from the central bank. “I would be concerned by disorderly conditions in markets or a persistent tightening in financial conditions that threatens the achievement of our goals,” Mr. Powell said Thursday. He added that the Fed is looking at “a broad range of financial conditions,” rather than a single measure. “If conditions do change materially, the [Fed’s rate-setting] committee is prepared to use the tools that it has to foster achievement of its goals,” Mr. Powell said. Mr. Powell said last week that the Fed doesn’t foresee lifting its benchmark fed-funds rate from near zero until three conditions have been met: a broad range of statistics indicate that the labor market is at maximum strength, inflation has hit its 2% target, and forecasters expect inflation to remain at that level or higher.

Mr. Powell said it’s “highly unlikely” that the Fed’s goal of maximum employment will be reached this year. But he was less clear about whether the economy could show enough improvement this year for the Fed to start reducing its monthly asset purchases.

“I’ve so far been able to not reduce it to an estimate of time. I mean, that will come, I think, when we can see that,” Mr. Powell said, referring to the standard that the Fed wants to meet before scaling back its asset purchases.

farm employment in the United States increased by 379,000 in February, according to data from the US Bureau of Labor Statistics on Friday. The figure exceeded expectations which hovered at around 200,000. The unemployment rate was little changed compared to the previous month at 6.2%, as well as the number of unemployed persons, at 10 million. The number of persons on temporary layoff fell by 517,000 in February to 2.2 million, although it is still 1.5 million higher on a yearly basis. The number of long-term unemployed was reported at 4.1 million, little changed from January, but up by 3 million over the year. The labor force participation rate remained at 61.4% in February.

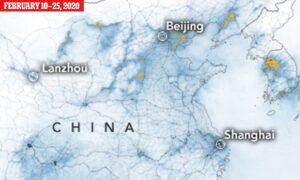

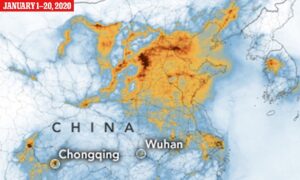

The coronavirus may have originated in China but its economic impact is being felt most acutely elsewhere. From Europe to North America, advanced nations are battling to contain a resurgence in infection rates and are bracing themselves for double-digit falls in output this year. They can only look with envy to China, where the economy has already recovered. Here is picture during lockdown”

No business during lockdown no smog

China did it right shit it down completley and totally….. test the shit out of everyone and only open up once the plague is under control. See how China loofs once it reopened:

President Joe Biden and federal health experts hit back Wednesday against Texas and Mississippi dropping their Covid-19 business restrictions and mask mandates, with Biden criticizing the decisions as “a big mistake,” joining a chorus of public health experts and officials who have spoken out against the orders being lifted while cases remain high and coronavirus variants spread. With the U.S. on the “cusp” of widespread vaccinations, the “last thing” it needs is “Neanderthal thinking that ‘in the meantime everything’s fine, take off your mask, forget it,’” Biden told reporters Wednesday, after White House Press Secretary Jen Psaki criticized the decision at an earlier press briefing, saying, “This entire country has paid the price for political leaders who ignored the science when it comes to the pandemic.” Dr. Anthony Fauci also criticized the states’ decisions as “ill-advised” and “really quite risky” at a town hall Wednesday with the United Food and Commercial Workers International Union, noting that in the past when cases have plateaued as they are now, “when you pull back on measures of public health, invariably you’ve seen a surge back up.” “The CDC have been very clear that now is not the time to release all restrictions,” Centers for Disease Control and Prevention Director Dr. Rochelle Wallensky said at a briefing Wednesday about the dropped measures, noting residents are “empowered to do their own thing here” by continuing to wear a mask and social distance “regardless of what the state decides.” The comments follow a series of high-profile figures who spoke out against Texas Gov. Greg Abbott’s decision Tuesday: Texas politician and former Rep. Beto O’Rourke slammed the move as a “death warrant for Texans,” while Rep. Alexandra Ocasio-Cortez (D-N.Y.) said Texas’s dropped restrictions “endangers the entire country and beyond.” Local leaders throughout Texas also criticized Abbott, with San Antonio Mayor Ron Nirenberg saying lifting the measures is a “huge mistake” akin to “cut[ting] off your parachute just as you’ve slowed your descent.”Health officials in Texas have also responded to the governor’s decision with outrage: Houston Health Department official Dr. David Persse said Tuesday he was “at a bit of a loss for words,” and Memorial Hermann Health System CEO Dr. David Callender told KHOU11, “I think the typical response I’ve heard today from our people is, what is he thinking?”

“It’s critical, critical, critical, critical that they follow the science” by wearing a mask, washing hands and social distancing, Biden told reporters Wednesday. “I know you all know that, but I wish the heck some of our elected officials would.”

Abbott announced Tuesday that all restrictions on businesses in the state and the statewide mask mandate will lift starting March 10 as cases in the state have gone down, declaring, “It is time to open Texas 100%.” Mississippi Gov. Tate Reeves also announced Tuesday his state would end its Covid-19 restrictions and mask mandate, which only applied to certain counties, as well. The decisions are part of a broader trend of states lifting or easing restrictions as Covid-19 cases have dropped nationwide. These steps have been taken over the objection of health officials, who have warned against relaxing restrictions while more transmissible coronavirus variants spread nationwide. Wallensky noted last week that the recent decline in cases now appears to be plateauing as variants have taken hold, calling the new trend a “very concerning shift” in the course of the pandemic. As coronavirus variants remain a concern, a February study found that Houston was the first city in the country to record every major variant that has been documented by genome sequencing so far. The study found 28 cases linked to variants, including the strains that were first identified in the United Kingdom, South Africa and Brazil.